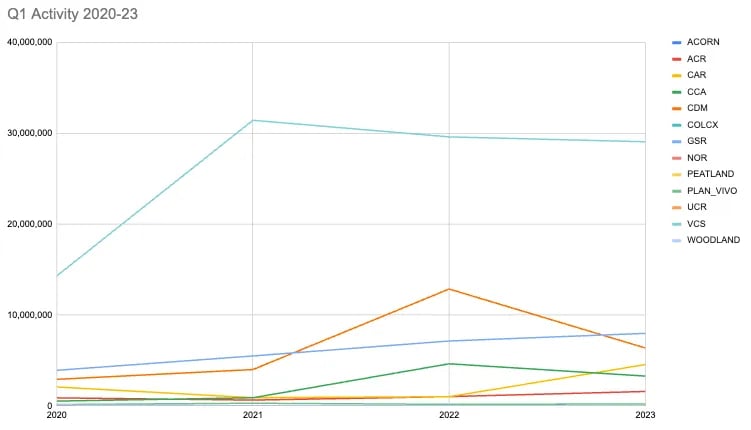

Despite the negative press around forestry projects on Verra, the most prominent carbon offsetting standard, Q1 2023 saw a 36% increase in retirements from those projects.

Retirements rose from just over 10m tCO2e to 14m tCO2e; projects that list REDD as their sole AFOLU Activity on Verra also saw a rise in retirements, from 5.8m tCO2e to 9.5m tCO2e. The 14m mark for Verra forestry was lower than 19m tCO2e retired in Q1 2021.

All data points in this article exclude credit tokenizations.

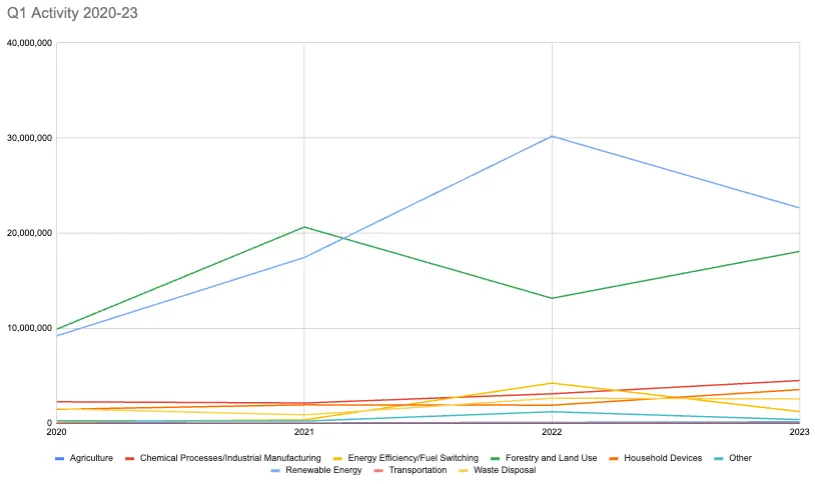

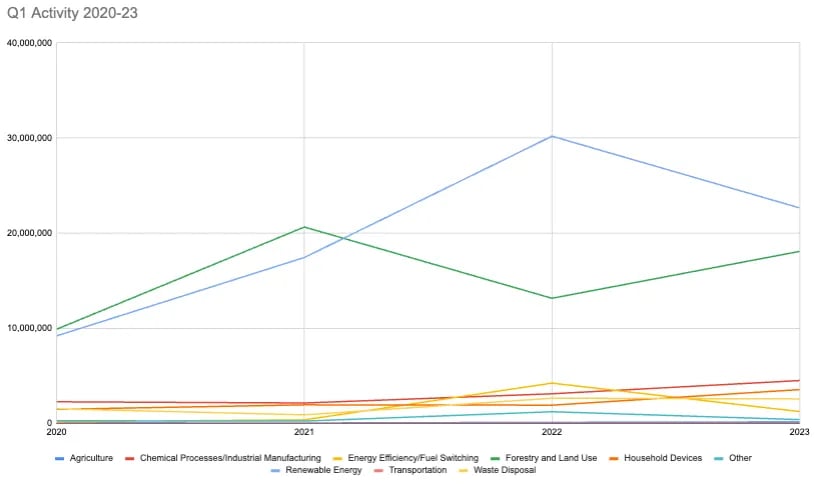

Overall activity in the market fell by 6%, with retirements falling from 57m to 54m tCO2e year on year.

Renewable energy credits saw a big fall since last year, though the number of retired credits was still higher than in 2021.

Prices have fallen quite a bit in the last two quarters: they sat at around $7 per ton in Q4 2022, and have come down to $5.70 in Q1 this year. (This pricing data attempts to capture an “average” retirement in the market, based on market activity, with credits from certain sectors or registries commanding a lower or higher price.)

At a registry level, nearly all registries have either mostly kept up with their previous year’s total, or saw a gain. The major exception here was CDM, which saw the number of credits voluntarily retired on its platform fall in half, from over 12m to 6m tCO2e.

The relatively healthy offsetting activity may be explained by a few factors, including:

- companies are brushing off concerns raised by the press,

- companies are taking advantage of the lower prices in the market, or

- retirements are taking place after budget had already been allocated in the previous year — suggesting future quarters may be less robust.

Our subscribers can log in to see more data here; our dashboard demo is here.