-1.jpg)

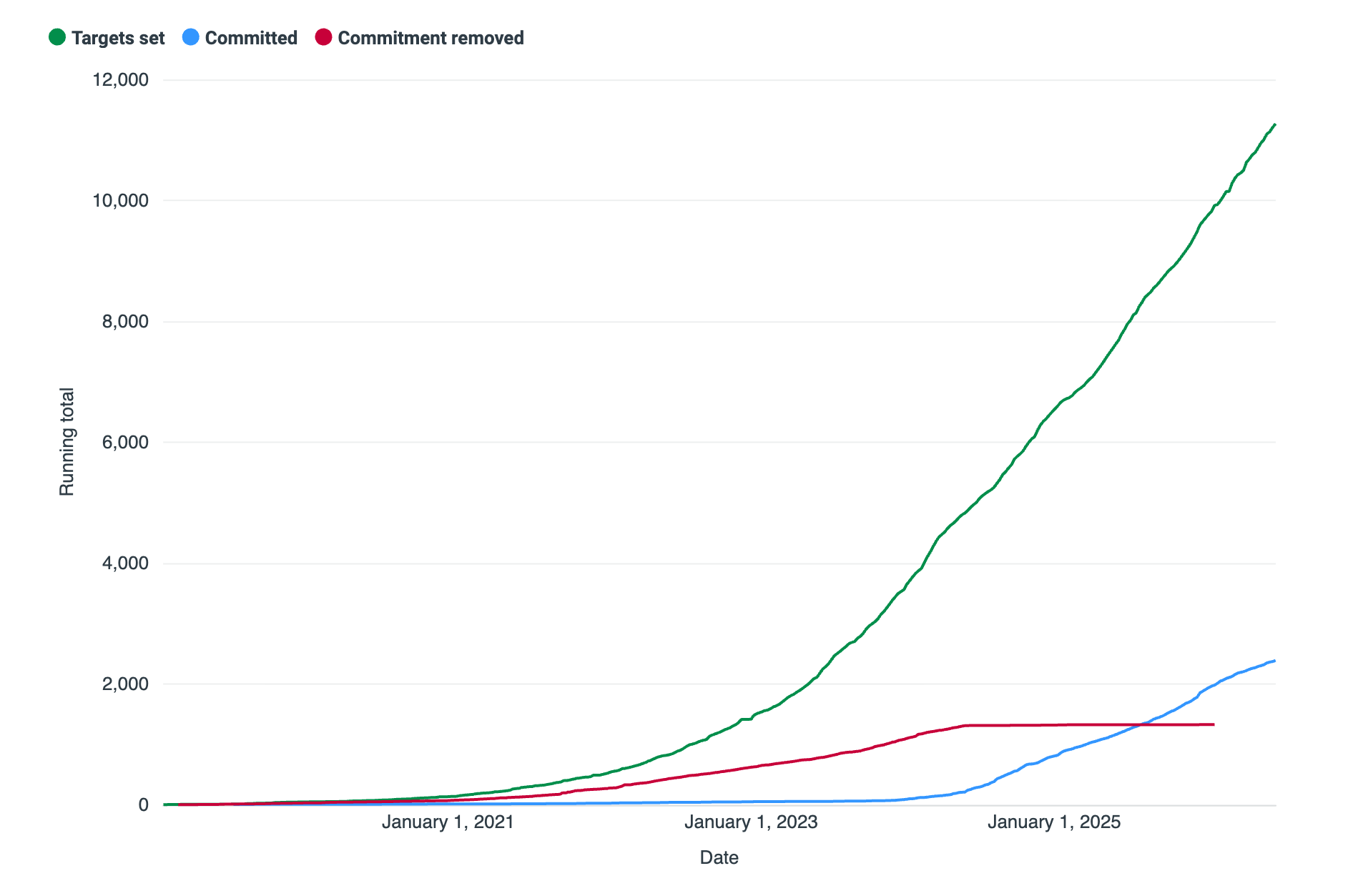

The Science Based Targets initiative (SBTi) published version 2.0 of its Corporate Net-Zero Standard in June 2026. With 11,278 companies with committed and validated targets (+8200 with validated targets, +1900 with net zero targets), the new standard introduces differentiated, context-specific approaches for companies looking to scale climate action consistent with meeting their net zero targets by 2050 or sooner.

SBTi corporate climate commitments: targets set, committed and removed, 2019-2026

The new framework: OER

The use of high-integrity carbon credits have been formally introduced under a framework called Ongoing Emissions Responsibility, or OER. This recognition of carbon credits as a tool for companies taking financial responsibility for the emissions they continue to produce while reducing is a structural shift from the SBTi’s historic position. Under V1, credit use was loosely categorized as Beyond Value Chain Mitigation, yet remained unrecognized and undefined. Under V2.0, OER is a structured three-tier program with public recognition on the SBTi Dashboard and a mandatory threshold from 2035 for Category A companies.

The three tiers are:

- Engaged (1% of total ongoing scope 1, 2 and 3, with a minimum recommended price point of $20/t),

- Advanced (10% of total ongoing emissions, with a mandatory $20/t price floor, and

- Leadership (100% of total ongoing emissions, with a mandatory $80/t price floor with both credits and contribution budget required.

Under this standard, companies can leverage carbon offsets as part of their decarbonization strategies, and the reputational benefits can pull companies up the tiers over time. All three tiers are also eligible for REDD and avoidance credits. The credit-type restriction only applies to the separate C45 neutralization mechanism, which governs hard-to-abate residual emissions at a company's net-zero year, a different, smaller pool which is not covered extensively here.

What OER means for the VCM: what the data shows

Modeling 1,275 of SBTi-validated companies finds that they represent a combined projected ongoing emissions of 7.09 Gt in 2025 (AlliedOffsets' forward emission forecast for these companies based on their current reduction trajectories). In 2025, those companies retired 15.22 Mt of credits, and under the OER criteria they fall below the first tier (Engaged, 1% of Scopes 1, 2 and 3) as those credits make up only 0.22% of their emissions base (71Mt). This represents a 4.6-times gap between current behaviour and higher ambition.

For context, the entire VCM retired 217.3 Mt in 2025. Full Engaged compliance (tier 1) of the 1,275 company cohort at 71Mt would represent roughly a third of the whole market. When scaled to all 11,278 companies with validated targets, the annual Engaged demand ceiling reaches 622 Mt - nearly three times the market. This should be treated as an upper bound, and the modeled cohort skews toward larger, better disclosing companies than the full universe.

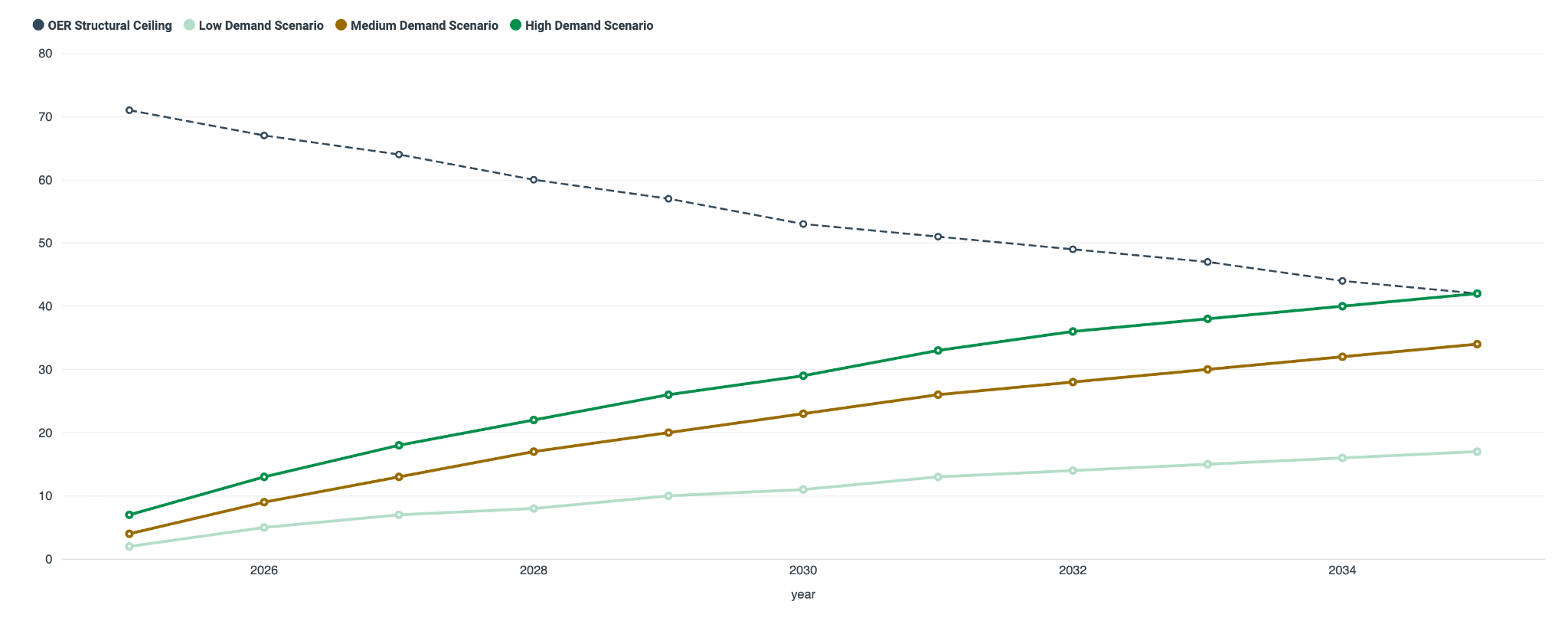

However, as the OER is calculated as a percentage of ongoing emissions, and because those emissions are meant to fall as companies reduce, the +1000 company cohort ceiling shrinks from 71Mt in 2025 to 42Mt in 2035. This structural dynamic means that OER does not create rising demand in a flat market - and demand only rises if there’s an accelerating adoption rate.

The Price constraint

Adoption of carbon credit usage will be dependent on many factors, including price. Assessing a subset of set internal carbon prices (ICPs) highlights a signal - 61% of validated companies have set an ICP at $15/t, which falls below the recommended $20/t Engaged floor, and far below the $80/t Leadership floor. These companies are predominantly Consumer Goods companies, pointing to an inherited sector benchmark rather than deliberate strategy. Technology and Financial Services companies average above $80/t and are structurally positioned to engage at Leadership tier today. Many high-emitting sector companies, across Industrials, Materials and Chemicals, and Food, have yet to disclose ICPs.

The ICP is both a price, and a budget signal. The OER contribution budget mechanism works as: ICP × covered emissions × tier coverage ratio = the capital a company is authorized to deploy on OER. At $15/t, that budget is below the standard's own recommended floor before a single credit is purchased. Tracking ICP revision over time will continue to be an informative indicator of VCM demand growth for scenario planning.

Short-term outlook (2025-2035)

Based on observed ICP behaviour, AlliedOffsets models three adoption paths for the 1,275-company cohort:

- Low - average ICPs stay at $15/t, we are likely to see minimal voluntary engagement. Annual demand for the cohort reaches 11Mt by 2030, 17Mt by 2035. Cumulative 2025-2035: 118Mt.

- In the Mid scenario, moderate ICP adjustment, companies beginning to position ahead of 2035/ Annual demand for the cohort would reach 23Mt by 2030, 34 Mt by 2035. Cumulative 2025-2035: 236Mt.

- In the High scenario, where we see a highly engaged voluntary cohort plus companies preparing for mandatory compliance. Annual demand reaches 29Mt by 2030, 42 Mt by 2035. Cumulative 2025-2035: 304Mt.

The current data, 0.22% retirement rate and $15/t modal ICP, puts the market in the Low scenario. Moving to Mid requires the majority of Consumer Goods, Fashion, and Construction companies to revise ICPs upward. There is currently no evidence that this is happening.

VCM demand scenarios vs OER structural ceiling, 2025-2035

What this means for credit types

The standard's formal recognition of carbon credits is good news for the VCM broadly, but the architecture creates differentiation within it.

For REDD and nature-based avoidance credits: OER eligibility is indefinite - there is no phase-out in 2035. The C45 removal requirement applies only to residual neutralization at net-zero year, not to OER. The structural pressures on REDD are market-driven rather than regulatory. At $5–15/t, REDD prices below the $20/t contribution budget floor, creating portfolio logic that favours higher-priced credit types among the most engaged buyers, particularly those operating at Advanced and Leadership tier. The investment case problem for conservation finance is not a cliff in 2035 but a progressively weakening relative demand signal across the 20–30 year project horizons that long-duration financing requires.

For removal credits: the standard's visible quality hierarchy, with long-lived removals (activities with +200 year permanence, e.g. Direct Air Capture, Bio-energy Carbon Capture and Storage) sitting at the top as they address residual emissions post-2035 under what is called the c45 neutralization pool, followed by short-lived removals such as nature based removals. Companies at Leadership ICP ($80/t+) are already active in CDR procurement, and as the 2035 mandatory threshold approaches, this cohort will expand.

For high-integrity avoidance credits (ICVCM CCP-approved, with verified additionality and no compliance double-counting): these sit in the strongest position within the OER-eligible pool. They satisfy C42's integrity requirements, and price above non-labelled credits in terms of current buyer preferences. Companies that have actively declared they plan to use credits are the near-term buyers for this tier.

Takeaways

While V2.0 does lay a foundation for short to medium term VCM growth, stopping short of mandating the use of credits prior to 2035 weakens it as a strong demand signal. One key factor which is worth tracking is whether companies revise their Internal Carbon Prices upwards, and we see greater adoption of targets, in parallel with more companies taking action to meet the minimum 1% Engaged OER tier ceiling.

Credits that can demonstrate quality commensurate with a $20-80/t contribution budget, with clear additionality, verifiable integrity, and alignment with buyer sector supply chains, are structurally positioned for the buyers who are actually moving. While the cohort may be small today, how fast it grows depends almost entirely on whether corporate ICPs trend upwards.

All figures confirmed from live AlliedOffsets Premium Dashboard queries, June 2026. SBTi Corporate Net-Zero Standard V2.0, June 2025.