As the voluntary carbon market (VCM) continues to expand, participants are faced with a variety of risks that can affect the success and credibility of their projects. Among these, key concerns include invalidation risk, political risk, reputational risk, price risk, non-delivery risk, reversal risk, and counterparty risk. These risks arise at different stages of a carbon project’s lifecycle, impacting not only developers but also buyers and intermediaries.

The latest World Bank’s State and Trends of Carbon Pricing report highlights that the presence of these risks has prompted the emergence of environmental service providers who are stepping in to spotlight these vulnerabilities, de-risk transactions, and incentivize more investments in carbon markets. We at AlliedOffsets provide data and intelligence to help market participants navigate the uncertainties of carbon projects while offering the tools to manage these complex risks effectively.

Political Risks in Carbon Markets: A Growing Concern

Among the most significant challenges in voluntary carbon markets is political risk, which stems from the possibility that carbon projects may be impacted by government interventions. Political risk can manifest in various ways, often leading to disruptions in carbon market transactions and eroding investor confidence.

Although national carbon market regulations remain sparse, development is ongoing. In the absence of fully matured and consistent regulation, carbon-related policies, which establish clear carbon rights and recognize voluntary carbon credits, are critical for fostering trust and participation in the market. Without this regulatory clarity, the risks of participating in voluntary carbon markets remain elevated.

Policy Reversals: A Threat to Investor Confidence

One specific form of political risk that has been particularly disruptive is policy reversal. Governments may reverse prior commitments, such as land concessions for carbon projects, which can have far-reaching consequences. When such reversals occur, they undermine investor confidence, decrease demand for credits, and increase reputational risks for buyers. Projects that were once seen as promising can suddenly lose their value or become non-compliant with new regulations, leaving both developers and investors at a loss.

Additionally, the evolving international climate policy landscape adds to the uncertainty. As negotiations under Article 6 of the Paris Agreement continue, particularly at COP29 later this year, the issue of revoking correspondingly adjusted credits remains a hot topic. Changes to these rules could dramatically affect the legitimacy and tradability of carbon credits, causing ripple effects throughout the market.

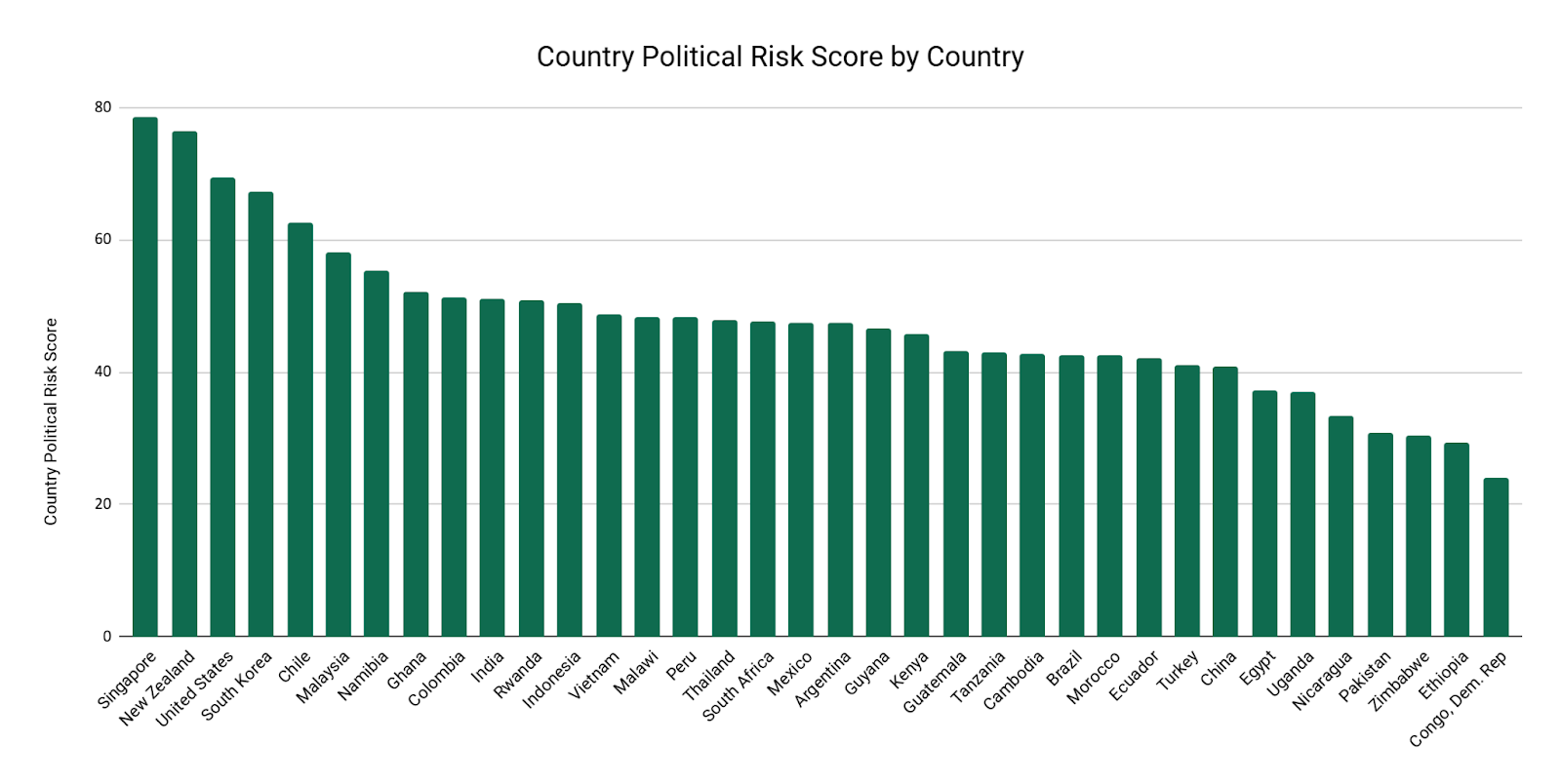

Introducing the AlliedOffsets Country Political Stability Index

To support stakeholders in the market we have devised a rating which assesses country-level political risk to investments, including within domestic voluntary carbon markets. The score integrates a weighted cumulative score, taken from ten risk metrics from appropriate third-party sources, and is updated annually. It ranks countries from high stability (or low risk) (61-100), medium (41-60) and low stability (or high political risk) (0-40), where higher scores suggest a safer, more predictable environment for investments and economic activities.

Indicators were selected from third-party sources, normalised out of 100, and then weighted based on perceived importance and then aggregated to come up with scores out of 100. All political risk scores are to be updated annually.

Methodology & Score Components

|

Indicator name |

Definitions |

Source |

Score metrics |

Weight |

|

Government stability, international conflicts, political violence and terrorism, social unrest, military coups etc. |

World Bank Governance Indicators |

-2.5 (Weak) to 2.5 (Strong) |

15% |

|

|

Quality of public services, civil service, policy formulation and implementation, credible government commitment |

World Bank Governance Indicators |

-2.5 (Weak) to 2.5 (Strong) |

15% |

|

|

Ability to formulate and implement sound policies, regulations that promote private sector development |

World Bank Governance Indicators |

-2.5 (Weak) to 2.5 (Strong) |

10% |

|

|

Legal rights for borrowers and lenders: secured transactions, credit information |

World Bank Governance Indicators |

0=weak legal rights to 12=strong legal rights |

10% |

|

|

Quality of contract enforcement, property rights, likelihood of crime and violence |

World Bank Governance Indicators |

-2.5 (Weak) to 2.5 (Strong) |

10% |

|

|

Level of perceived corruption, transparency and accountability of institutions |

Transparency International |

0 (high perceived corruption) to 100 (low perceived corruption) |

10% |

|

|

Economic freedom based on property rights, government integrity and regulatory efficiency |

The Heritage Foundation |

0 (low economic freedom) to 100 (greater economic freedom) |

10% |

|

|

Societal cohesion (security, elites), economic fragility (decline, poverty, inequality), political fragility (legitimacy, services, rights, law), social (demographics, refugees or displacement). |

The Fund for Peace (FFP) |

0 (least vulnerable) to 120 (most vulnerable, fragile) |

8% |

|

|

Assesses political rights and civil liberties in a country |

Freedom House |

0=unfree, 60=highest civil and political freedoms |

6% |

|

|

Relative peacefulness based on domestic and international conflict, safety and militarization. |

Institute for Economics and Peace |

1 (most peaceful) to 5 (least peaceful) |

6% |

The rating currently covers 38 countries, including Guyana, United States, Colombia, China and more. We have added this score to support our dashboards assessing investment risks, and to complement a host of new indicators related to policy-side tools to provide more clarity to the VCM space.