The carbon removal market maintained steady activity in February, with biochar emerging as the dominant pathway across offtakes, investment, and issuance.

While total offtake volumes remained broadly stable month-on-month, both investment and issuance declined. Despite this slowdown, activity continued across several carbon removal pathways, reflecting ongoing engagement from both buyers and project developers.

Retirements rebounded strongly during the month, increasing 46% month-on-month and pushing the retirements-to-issuance ratio up to 55%. Although retirements still lag new supply, this represents a gradual improvement in demand absorption compared to January.

The month also saw new buyers entering the market, including luxury fashion group Tapestry, highlighting the continued expansion of the corporate buyer base for carbon removals.

These developments also reflect broader questions shaping the market today, including how much carbon removal costs, whether durable carbon removal technologies like direct air capture can scale, and how emerging approaches such as enhanced rock weathering and ocean alkalinity enhancement fit into the global CDR deployment pathway.

Monthly highlights:

- Offtake: 196,200 credits | Deals: 5 (MoM - 9%).

- Investment: $39.4 Million (MoM - 30%).

- Issuance: 40,010 credits (MoM - 45%).

- Retirements: 22,103 credits (MoM + 46%).

Carbon Removal Offtakes and Corporate Purchases

Offtake activity totalled 196,200 credits across five disclosed transactions during the month.

Biochar dominated total contracted volume. The largest deal in February was a 105,000 credit agreement between aviation companies and Exomad Green, highlighting growing interest from aviation stakeholders in durable carbon removals.

Climeworks also signed a multi-year agreement with Truecoco Ghana Ltd for 90,000 biochar credits. These credits will be incorporated into the Climeworks portfolio, allowing them to be sold onward to end buyers as part of the company’s carbon removal offering.

Other deals highlighted continued diversification of buyer interest across pathways. Zurich Insurance signed a 1,200 ton direct air capture agreement with Parallel Carbon, while Rothschild & Co signed an agreement with OCO Technology for mineralization-based removals.

Tapestry also announced a partnership with Climeworks, securing access to carbon removals through the company’s portfolio.

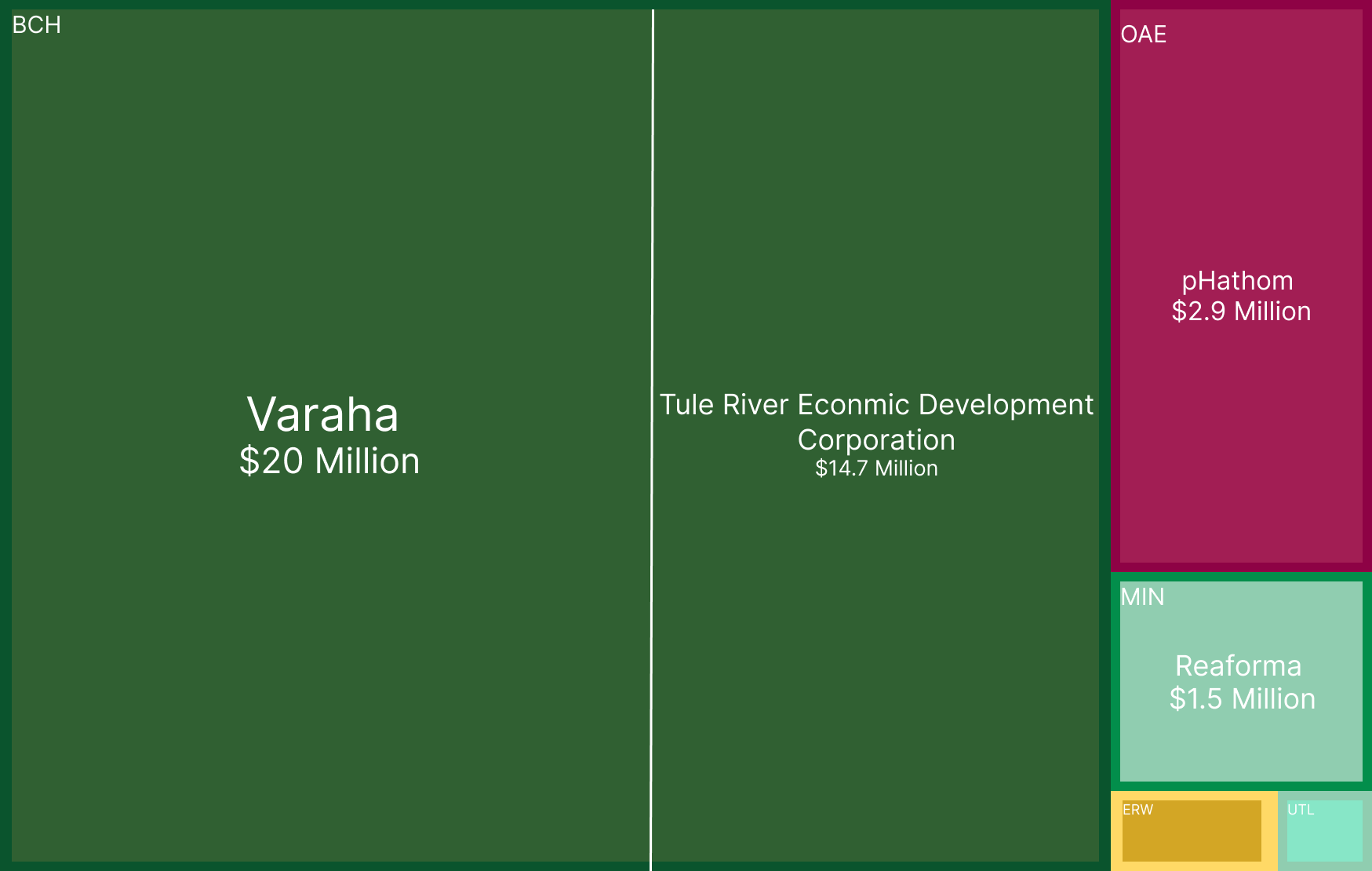

Investment

Total disclosed investment reached $39.4 million during the month, down 30% month-on-month.

Biochar projects captured the majority of funding. Varaha raised $20 million, while the Tule River Economic Development Corporation secured $14.7 million to support biochar deployment.

Other notable investments included $2.9 million raised by ocean alkalinity enhancement developer pHathom.

Smaller early-stage investments were also recorded across several emerging pathways, including enhanced rock weathering developers Mati and InPlanet, CO2 utilization company UP Catalyst, and mineralization-focused developer Reaforma.

Overall, investment activity declined compared with the previous month but remained distributed across a range of carbon removal technologies.

Issuance : Biochar Carbon Removal Credits Lead Supply

Total issuance reached 40,010 credits during the month, down 45% month-on-month.

Issuance activity was overwhelmingly dominated by biochar projects, which accounted for the vast majority of credits generated.

Exomad Green led issuance with over 20,000 credits, followed by Varaha with nearly 8,000 credits. Biochar developers collectively represented the largest share of supply entering the market.

Bio-based carbon storage projects also contributed to issuance, with developers such as Vaulted Deep, Graphyte, and Woodcache generating credits under biomass storage pathways.

Retirements

Total retirements reached 22,103 credits during the month, increasing 46% month-on-month.

Despite this increase, retirements continued to lag new supply. The retirements-to-issuance ratio stood at 55%, indicating that credit utilization remains below the level of new credits entering the market.

However, the share of retirements compared to January increased by 34%, suggesting improving demand absorption during the month.

To learn more about CDR and broader carbon market trends, explore our latest insights and reports here.