When a company begins its transition to carbon neutrality, the first thing it must do is understand the amount of carbon it emits.

Carbon accounting is the process of monitoring greenhouse gas (GHG) emissions across the value chain. This process is crucial, as it increases the company’s responsibility and serves as a starting point to set themselves targets aligned with the Paris Agreement and to monitor their progress towards the goal.

The World Resources Institute (WRI) as well as the World Council for Sustainable Development (WBCSD) have had a significant role in establishing the scopes for carbon accounting in the GHG Protocol’s Corporate Standard. ‘Scopes’ distinguish between direct and indirect emissions, which account for different stages of a product’s production process and corporate value chain. The scopes are explained thus:

- Scope 1 represents the direct GHG emissions caused by activities that are owned and controlled by the organisation. Such as the emissions from a vehicle owned by the company. They are usually the most straightforward to calculate as the sources are finite and known.

- Scope 2 are the indirect emissions from electricity, which represent the emissions caused by the production of electricity the organisation has used. An example would be a power plant the organisation has bought energy from. These emissions are also relatively easy to measure as electricity production is a standardised process and the organisation knows how much they have consumed over a period of time.

- Scope 3 represents all the other indirect emissions from sources the company does not own nor control. Scope 3 often accounts for most of an organisation’s emissions as it includes the whole supply and value chain. The supply chain includes product’s raw materials, the use of the products, transportation related to products and people. Given how broad scope 3 emissions are, they are the most complicated to assess but nonetheless crucial to be measured and reduced as often scope 3 emissions contribute the most to corporate carbon footprint, for example in the oil and gas industry where it accounts for fossil fuel combustion. But, it is key to measure and reduce them, as scope 3 emissions often contribute the most to corporate carbon footprint.

There have been several attempts at putting in place international standards for carbon accounting. For instance, the International Organisation for Standardisation (ISO) has created standards like the ISO 14064, which sets principles for the quantification and reporting of carbon emissions and details the development, management, and verification of a company’s emissions. They recently released ISO 14067 in an effort to create an international standard for evaluating the carbon footprint of products. Another commonly used standard is GRI Standard 305 on emissions, which provides guidance on how emissions should be measured and reported to give enough details to stakeholders on the company’s climate-related activities.

Some of the companies featured in our buyer matching process (previous blog: Which Industries Are Most Involved in the Voluntary Carbon Market?) adhere to the guidelines described above and have attempted to quantify their GHG emissions and are open about their attempts to reduce emissions related to all three scopes.

Case study: Shell

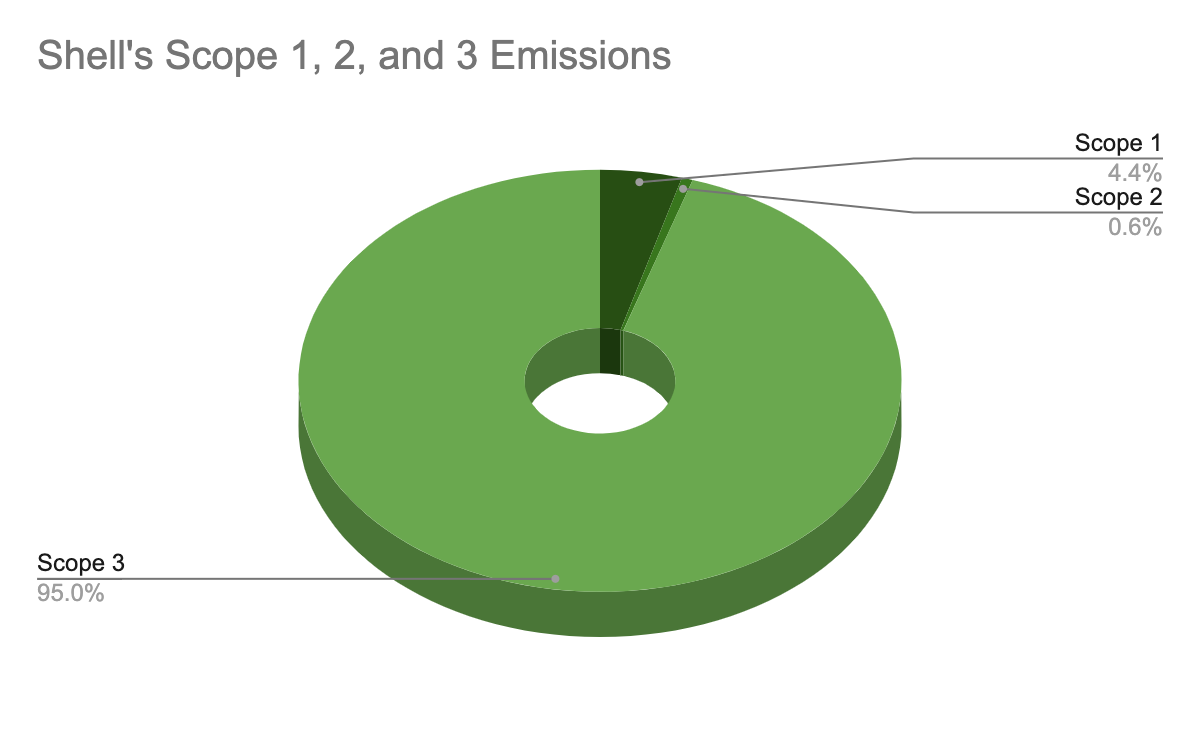

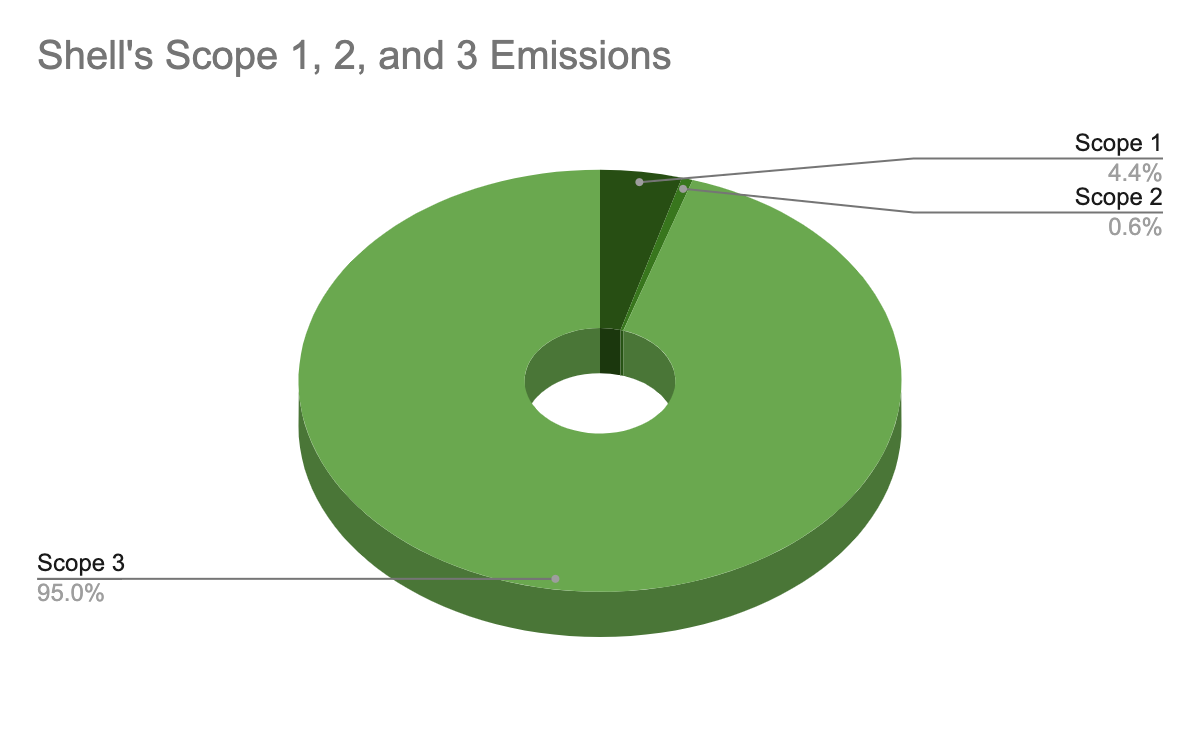

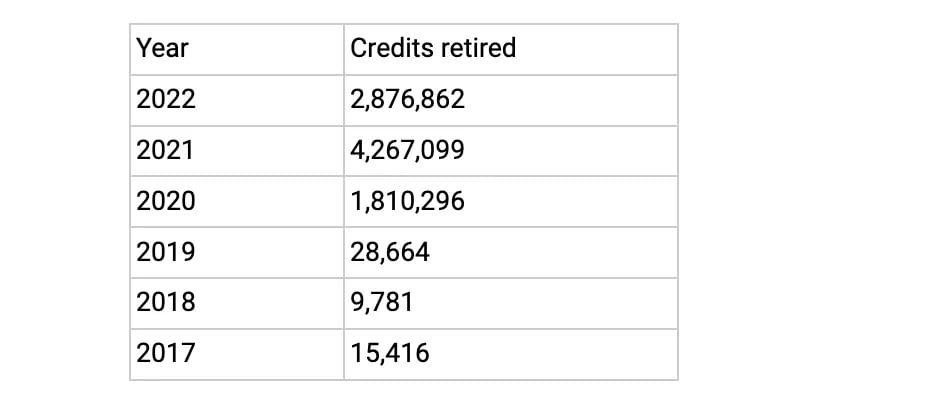

In 2021, Shell’s emissions were — Scope 1: 60 million tCO2, Scope 2: 8 million tCO2; Scope 3: 1.3 billion tCO2. Over the same period, the company retired 9 million carbon credits, which is a very small fraction of its emissions. In fact, in 2021 Shell offset about 0.31% of its total emissions for the year. (And 6.3% of their Scope 1 and 2 emissions.)

The retired credits come from projects such as Cordillera Azul in Peru and Kasigau in Kenya, among others; most retirements also came from forestry and land use projects (based on AlliedOffsets data of publicly announced retirements).

Shell has committed to reduce their Scope 1 and 2 emissions by 50% by 2030 compared to the company’s 2016 emissions. They also aim at net zero emissions generated by Shell’s operations by 2050. This implies Shell has not set any target to reduce their scope 3 emissions which are significantly higher than scope 1 and 2 combined.

For more information, check out our demo dashboard here.